One Big Beautiful Bill Act (OB3 or OBBBA), sometimes also referred to as the "Working Families Tax Cuts" Act, which was signed into law on July 4, 2025, through the budget reconciliation process.

As this legislation contains significant provisions that reshape student financial aid, this page is dedicated to updating student and parent borrowers on what these changes mean for them.

Beginning July 1, 2026, changes to the law affect how much parents can borrow from the Parent PLUS Loan program for their children’s college education and the available repayment options for those loans. There are no changes to how much undergraduate students can borrow.

New federal borrowing limits cap the Parent PLUS Loan at $20,000 per year and $65,000 in total, but the law allows for a time-limited exception to new loan limits for currently-enrolled students. In order for Parent PLUS Loan borrowers to not be subject to the new loan limits:

• The student must remain continuously enrolled in the same program of study at the same institution as they were enrolled as of June 30, 2026, AND

• The parent borrower must have had a Parent PLUS Loan disbursed for that same program before July 1, 2026, OR

• The student must have had a Direct Loan (subsidized or unsubsidized) disbursed for that same program before July 1, 2026.

If the above requirements are met, the new Parent PLUS Loan limits do not apply while the student is completing their program, for up to 3 years, provided the student remains continuously enrolled (i.e., does not withdraw or otherwise cease enrollment outside of scheduled breaks or non-required terms, such as summer).

Parents of current students who do not currently meet these criteria can still qualify for this limited exception to the new loan limits if:

• The parent borrows a Parent PLUS Loan prior to July 1, 2026, OR

• The student borrows a Direct Loan (subsidized or unsubsidized) prior to July 1, 2026.

What happens when students no longer qualify for the limited exception?

After three academic years, or earlier if the student withdraws or otherwise ceases enrollment from their current school or completes their program of study, Parent PLUS Loan borrowers become subject to the new $20,000 annual and $65,000 aggregate loan limits.

What if a Parent PLUS Loan borrower needs more than the annual borrowing limit, or reaches the aggregate limit before the student graduates?

Talk to the financial aid office about other financing options, like external scholarships, payment plans, or institutional or private loans.

Repayment Information

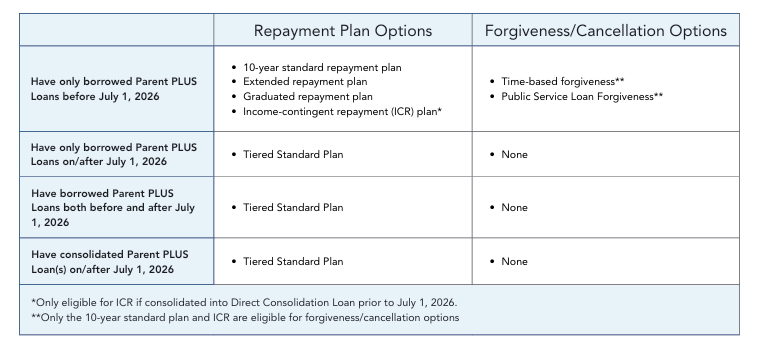

Any federal Parent PLUS Loans borrowed on or after July 1, 2026 (including federal consolidation loans that include Parent PLUS Loans) can only be repaid under a single new, fixed repayment plan. For Parent PLUS Loans taken out on or after July 1, 2026, the only repayment plan option available will be a new tiered standard repayment plan. The tiered standard repayment plan offers a fixed monthly payment over 10 to 25 years, based on the outstanding balance of the loan(s). This applies to parent borrowers with existing Parent PLUS Loans who borrow a new loan on or after July 1, 2026, as well, because the law requires that all Parent PLUS Loans be repaid under the same repayment plan.

Parents who currently have Parent PLUS loans in repayment and borrow a Parent PLUS Loan on or after July 1, 2026, will have all of their Parent PLUS Loans moved to the tiered standard repayment plan, potentially changing the monthly payment amount. Current Parent PLUS Loan borrowers may repay their loans under the following repayment plans until their loans are fully repaid, but only if they do not borrow new Parent PLUS Loans on or after July 1, 2026:

• 10-year standard repayment plan

• Extended repayment plan

• Graduated repayment plan

Parent PLUS Loan borrowers who consolidated their Parent PLUS Loans into a Direct Consolidation Loan before July 1, 2026, may repay their loans under the income-contingent repayment (ICR) plan through June 30, 2028, at which point that plan will sunset, and Parent PLUS Loan borrowers repaying under ICR will be moved to the income-based repayment (IBR) plan.

Parents who want access to an income-driven repayment plan and/or loan forgiveness for their Parent PLUS Loans must:

• Have consolidated their Parent PLUS Loans into a Direct Consolidation Loan prior to July 1, 2026 and are enrolled in the income-contingent repayment (ICR) plan prior to July 1, 2028 AND

• Not have borrowed a new Parent PLUS Loan on or after July 1, 2026.

Parent PLUS Loans and Public Service Loan Forgiveness (PSLF)

The new tiered standard repayment plan does not count as a qualifying repayment plan for PSLF purposes. As a result, borrowing a new Parent PLUS Loan on or after July 1, 2026, prevents borrowers from receiving PSLF, even if they have already made qualifying payments, as all Parent PLUS loans must be repaid under the new tiered standard repayment plan.

Parents who are planning to borrow a Parent PLUS Loan on or after July 1, 2026, but who want to preserve their eligibility for PSLF, may want to carefully consider other ways to help finance their dependent student’s education.

Beginning July 1, 2026, changes to the law affect how much parents can borrow from the Parent PLUS Loan program for their children’s college education and the available repayment options for those loans. There are no changes to how much undergraduate students can borrow.

There are new loan limits for the Parent PLUS Loan program:

• $20,000 per dependent student, per year (annual limit).

• $65,000 per dependent student, in total (aggregate limit).

Importance of planning accordingly

The new aggregate limit of $65,000 means that borrowing the annual maximum for a four-year undergraduate program will cause parents to reach the aggregate limit before the student completes their degree, leaving them without further access to the Parent PLUS Loan. On the Parent PLUS Loan application, parents should only select the “maximum amount” option if they wish to borrow the full $20,000 for the year. To ensure adequate Parent PLUS Loan eligibility for the duration of the student’s undergraduate program, parents should request a lesser amount on the application. For example, request $16,250 per year for total (aggregate) eligibility to be split equally for a four-year program.

What if a Parent PLUS Loan borrower needs more than the annual borrowing limit, or reaches the aggregate limit before the student graduates?

Discuss other financing options with the financial aid office, such as external scholarships, payment plans, institutional loans, or private loans.

Repayment Information

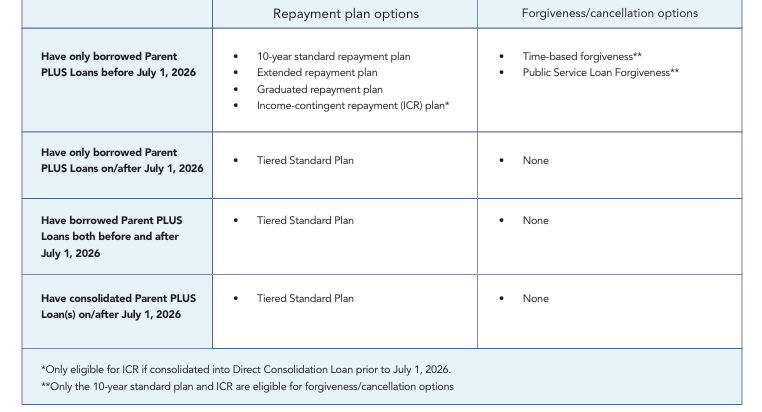

Any federal Parent PLUS Loans borrowed on or after July 1, 2026 (including federal consolidation loans that include Parent PLUS Loans) can only be repaid under a single new, fixed repayment plan. For Parent PLUS Loans taken out on or after July 1, 2026, the only repayment plan option available will be a new tiered standard repayment plan. The tiered standard repayment plan offers a fixed monthly payment over 10 to 25 years, based on the outstanding balance of the loan(s). This applies to parent borrowers with existing Parent PLUS Loans who borrow a new loan on or after July 1, 2026, as well, because the law requires that all Parent PLUS Loans be repaid under the same repayment plan. The tiered standard repayment plan offers a fixed monthly payment over 10 to 25 years, based on the outstanding balance of the loan(s).

Parents who currently have Parent PLUS loans in repayment and borrow a Parent PLUS Loan on or after July 1, 2026, will have all of their Parent PLUS Loans moved to the tiered standard repayment plan, potentially changing the monthly payment amount. Current Parent PLUS Loan borrowers may repay their loans under the following repayment plans until their loans are fully repaid, but only if they do not borrow new Parent PLUS Loans on or after July 1, 2026:

• 10-year standard repayment plan

• Extended repayment plan

• Graduated repayment plan

Parent PLUS Loan borrowers who consolidated their Parent PLUS Loans into a Direct Consolidation Loan before July 1, 2026, may repay their loans under the income-contingent repayment (ICR) plan through June 30, 2028, at which point that plan will sunset, and Parent PLUS Loan borrowers repaying under ICR will be moved to the income-based repayment (IBR) plan.

Parents who want access to an income-driven repayment plan and/or loan forgiveness for their Parent PLUS Loans must:

• Have consolidated their Parent PLUS Loans into a Direct Consolidation Loan prior to July 1, 2026 and are enrolled in the income-contingent repayment (ICR) plan prior to July 1, 2028 AND

• Not have borrowed a new Parent PLUS Loan on or after July 1, 2026.

Parent PLUS Loans and Public Service Loan Forgiveness (PSLF)

The new tiered standard repayment plan does not count as a qualifying repayment plan for PSLF purposes. As a result, borrowing a new Parent PLUS Loan on or after July 1, 2026, prevents borrowers from receiving PSLF, even if they have already made qualifying payments, as all Parent PLUS loans must be repaid under the new tiered standard repayment plan.

Parents who are planning to borrow a Parent PLUS Loan on or after after July 1, 2026, but who want to preserve their eligibility for PSLF, may want to carefully consider other ways to help finance their dependent student’s education.

Beginning July 1, 2026, changes to the law will affect the amount graduate students can borrow, the types of loans available, and their repayment options after graduation.

Starting July 1, 2026, the Graduate PLUS loan program will be eliminated unless students qualify for a limited exception. Students who currently depend on Grad PLUS loans to help pay for school should be sure they know whether they qualify for the exception and what conditions could lead to the loss of Graduate PLUS eligibility.

The annual Direct Unsubsidized Loan limit remains unchanged at $20,500. However, there is a new $100,000 cap on the amount students can borrow in total (aggregate) for a graduate degree program and a new lifetime federal loan limit of $257,500 for all Federal Direct student loans (excluding Parent PLUS loans) borrowed for all levels of study. Students who qualify for the limited exception, described below, that allows them to continue to borrow Graduate PLUS loans are also exempt from the new Direct Unsubsidized aggregate and lifetime limits.

Limited exception

The law allows some students to continue borrowing from the Graduate PLUS program without being subject to the new Direct Unsubsidized aggregate and lifetime borrowing limits under a limited exception through their time to completion, for a maximum of three years. Students may qualify for the limited exception if:

• They remain continuously enrolled in the same program of study at the same institution as they were enrolled as of June 30, 2026, AND

• They had a Direct Loan disbursed (Direct Unsubsidized or Graduate PLUS) for that same program before July 1, 2026.

Is there an opportunity to qualify for the limited exception for students who don’t currently meet the criteria?

Yes, taking out a federal student loan (Direct Unsubsidized or Graduate PLUS) before June 30, 2026, could help students keep access to Graduate PLUS Loans and the current aggregate and lifetime borrowing limits under the limited exception. However, borrowing just to “lock in” eligibility isn’t the right choice for everyone. Borrowing has long-term consequences, so talk with the financial aid office before deciding to borrow.

What happens when students no longer qualify for the limited exception?

After three academic years, or earlier if the student withdraws, ceases enrollment, or completes their program of study, they will no longer qualify for Graduate PLUS Loans and will become subject to the new aggregate and lifetime borrowing limits.

What options are available for students who need to borrow more than they are able through federal student loans?

Discuss other financing options with the financial aid office, such as scholarships, payment plans, institutional loans, or private loans.

If students enroll part-time in 2026-27 or future years, their federal Direct Unsubsidized and/or Graduate PLUS Loans (if they qualify to borrow a Graduate PLUS under the limited exception described above) must be prorated in accordance with changes to the law. Students thinking of enrolling part-time or dropping a class should talk to their financial aid office first to understand the implications.

Students who borrow a new federal Direct Loan on or after July 1, 2026, will be eligible for only two repayment plans:

- Tiered Standard Repayment

• Fixed monthly payments

• Repayment term lengths range from 10 to 25 years, depending on the amount borrowed. - Repayment Assistance Plan (RAP)

• Monthly payments based on income

• Loan forgiveness after 30 years of repayment

• Is a qualifying plan for Public Service Loan Forgiveness

All federal loans must be repaid using the same repayment plan. Students with older loans (borrowed before July 1, 2026) who take out new loans on or after that date will have to repay their loans under one of the two repayment options described above.

Students who do not borrow a new federal Direct Loan on or after July 1, 2026, may continue to access current repayment options, including:

• Standard (10-year), Graduated, or Extended Repayment

• Income-Based Repayment (IBR)

• Pay As You Earn (PAYE)*

• Income-Contingent Repayment (ICR)*

*The law sunsets the PAYE and ICR plans effective July 1, 2028. Borrowers who enroll in PAYE or ICR must switch to any of the other eligible plans listed before July 1, 2028, or they will be automatically moved into RAP. They may also access the new Repayment Assistance Plan (RAP) once it becomes available in July 2026.

Beginning July 1, 2026, changes to the law will affect the amount professional students can borrow, the types of loans available, and their repayment options after graduation.

Starting July 1, 2026, the Graduate PLUS loan program will be eliminated unless students qualify for a limited exception. Students who currently depend on Graduate PLUS loans to help pay for school should be sure they know whether they qualify for the exception and what conditions could lead to the loss of Graduate PLUS eligibility.

There is a new, higher annual Direct Unsubsidized Loan limit of $50,000. There is also a new cap of $200,000 on the amount students can borrow in total (aggregate) for a professional degree program and a new lifetime federal loan limit of $257,500 for all Federal Direct student loans (excluding Parent PLUS loans) borrowed for all levels of study. Students who qualify for the limited exception, described below, that allows them to continue to borrow Graduate PLUS loans are also exempt from the new Direct Unsubsidized annual, aggregate, and lifetime limits.

Who is considered a professional student?

Students in the following Belmont programs are considered professional students for purposes of federal student loan limits:

• Pharmacy (Pharm.D.)

• Law (LL.B. or J.D.)

• Medicine (M.D.)

Limited exception

The law allows some students to continue borrowing from the Graduate PLUS program without being subject to the new Direct Unsubsidized aggregate and lifetime borrowing limits under a limited exception through their time to completion, for a maximum of three years.

Students may qualify for the limited exception if:

• They remain continuously enrolled in the same program of study at the same institution as they were enrolled as of

June 30, 2026, AND

• They had a Direct Loan disbursed (Direct Unsubsidized or Graduate PLUS) for that same program before July 1, 2026.

The limited exception also maintains the current annual limit of $20,500 for Direct Unsubsidized Loans.

Is there an opportunity to qualify for the limited exception for students who don’t currently meet the criteria?

Yes, taking out a federal student loan (Direct Unsubsidized or Graduate PLUS) before June 30, 2026, could help students keep access to Graduate PLUS Loans and the current aggregate and lifetime borrowing limits under the limited exception. Remember, though, that students who meet the limited exception criteria maintain access to the Graduate PLUS loan program, but are limited to borrowing $20,500 annually from the Direct Unsubsidized Loan. Think of it as an all-or-nothing when it comes to qualifying for the new loan terms versus the old terms. Additionally, borrowing solely to “lock in” eligibility may not be the right choice for everyone. Borrowing has long-term consequences, so talk with the financial aid office before deciding to borrow.

What happens when students no longer qualify for the limited exception?

After three academic years, or earlier if the student withdraws, ceases enrollment, or completes their program of study, they no longer qualify for Graduate PLUS Loans and will become subject to the new annual, aggregate, and lifetime borrowing limits.

What options are available for students who need to borrow more than they are able through federal student loans?

Talk to the financial aid office about other financing options, like scholarships, payment plans, institutional, or private loans.

If students enroll part-time in 2026-27 or future years, their federal Direct Unsubsidized and/or Graduate PLUS Loans (if they qualify to borrow a Graduate PLUS under the limited exception described above) must be prorated in accordance with changes to the law. Students thinking of enrolling part-time or dropping a class should talk to their financial aid office first to understand the implications.

Students who borrow a new federal Direct Loan on or after July 1, 2026, will be eligible for only two repayment plans:

- Tiered Standard Repayment

• Fixed monthly payments

• Repayment term length ranges from 10 to 25 years, based on the amount borrowed - Repayment Assistance Plan (RAP)

• Monthly payments based on income

• Loan forgiveness after 30 years of repayment

• Is a qualifying plan for Public Service Loan Forgiveness

All federal loans must be repaid using the same repayment plan. Students with older loans (borrowed before July 1, 2026) who take out new loans on or after that date will have to repay their loans under one of the two repayment options described above.

Students who do not borrow a new federal Direct Loan on or after July 1, 2026, may continue to access current repayment options, including:

• Standard (10-year), Graduated, or Extended Repayment

• Income-Based Repayment (IBR)

• Pay As You Earn (PAYE)*

• Income-Contingent Repayment (ICR)*

*The law sunsets the PAYE and ICR plans effective July 1, 2028. Borrowers who enroll in PAYE or ICR must switch to any of the other eligible plans listed before July 1, 2028, or they will be automatically moved into RAP. They may also access the new Repayment Assistance Plan (RAP) once it becomes available in July 2026.

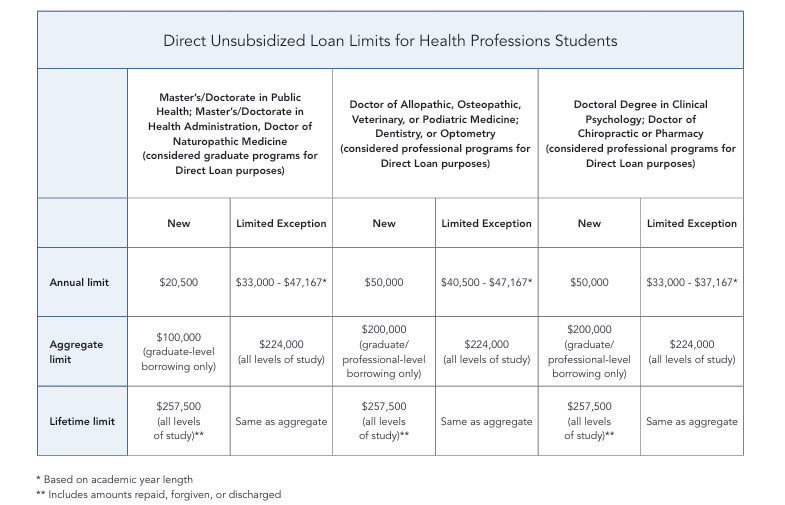

Beginning July 1, 2026, changes to the law will affect the amount of federal student loans health professions students can borrow, the types of loans available, and their repayment options after graduation.

Starting July 1, 2026, the Graduate PLUS loan program will be eliminated unless students qualify for a limited exception. Students who currently depend on Grad PLUS loans to help pay for school should be sure they know whether they qualify for the exception and what conditions could lead to the loss of Graduate PLUS eligibility.

There are also new Direct Unsubsidized Loan annual and total (aggregate) limits, based on whether students are considered graduate or professional students, and a new lifetime borrowing limit.

Some health professions students will see higher annual and aggregate Direct Unsubsidized Loan eligibility, while others will qualify for lower amounts.

Students who qualify for the limited exception, described below, that allows them to continue to borrow Graduate PLUS loans are also exempt from the new Direct Unsubsidized annual, aggregate, and lifetime limits.

Limited exception

The law allows some students to continue borrowing from the Graduate PLUS program without being subject to the new Direct Unsubsidized annual, aggregate, and lifetime borrowing limits under a limited exception through their time to completion, for a maximum of three years.

Students may qualify for the limited exception if:

• They remain continuously enrolled in the same program of study at the same institution as they were enrolled as of

June 30, 2026, AND

• They had a Direct Loan disbursed (Direct Unsubsidized or Graduate PLUS) for that same program before July 1, 2026

Is there an opportunity to qualify for the limited exception for students who don’t currently meet the criteria?

Yes, taking out a federal student loan (Direct Unsubsidized or Graduate PLUS) before June 30, 2026, could help students keep access to Graduate PLUS Loans and the current aggregate and lifetime borrowing limits under the limited exception. Remember, though, that students who meet the limited exception criteria maintain access to the Graduate PLUS loan, but are limited to borrowing the current Direct Unsubsidized Loan limits detailed above. Think of it as an all-or-nothing when it comes to qualifying for the new loan terms versus the old terms. Additionally, borrowing solely to “lock in” eligibility may not be the right choice for everyone. Borrowing has long-term consequences, so talk with the financial aid office before deciding to borrow.

Can students opt out of the limited exception eligibility if they prefer those annual and aggregate limits?

No, limited exception eligibility cannot be forfeited.

What happens when students no longer qualify for the limited exception?

After three academic years, or earlier if the student withdraws, ceases enrollment, or completes their program of study, they will no longer qualify for Graduate PLUS Loans and will become subject to the new annual, aggregate, and lifetime borrowing limits.

What options are available for students who need to borrow more than they are able through federal student loans?

Talk to the financial aid office about other financing options, like scholarships, payment plans, institutional, or private loans.

If students enroll part-time in 2026-27 or future years, their federal Direct Unsubsidized and/or Graduate PLUS Loans (if they qualify to borrow a Graduate PLUS under the limited exception described above) must be prorated in accordance with changes to the law. Students thinking of enrolling part-time or dropping a class should talk to their financial aid office first to understand the implications.

Students who borrow a new federal Direct Loan on or after July 1, 2026, will be eligible for only two repayment plans:

- Tiered Standard Repayment

• Fixed monthly payments

• Repayment term lengths range from 10 to 25 years, depending on the amount borrowed.

2. Repayment Assistance Plan (RAP)

• Monthly payments based on income

• Loan forgiveness after 30 years of repayment

• Is a qualifying plan for Public Service Loan Forgiveness

All federal loans must be repaid using the same repayment plan. Students with older loans (borrowed before July 1, 2026) who take out new loans on or after that date will have to repay their loans under one of the two repayment options described above.

Students who do not borrow a new federal Direct Loan on or after July 1, 2026, may continue to access current repayment options, including:

• Standard (10-year), Graduated, or Extended Repayment

• Income-Based Repayment (IBR)

• Pay As You Earn (PAYE)*

• Income-Contingent Repayment (ICR)*

*The law sunsets the PAYE and ICR plans effective July 1, 2028. Borrowers who enroll in PAYE or ICR must switch to any of the other eligible plans listed before July 1, 2028, or they will be automatically moved into RAP. They may also access the new Repayment Assistance Plan (RAP) once it becomes available in July 2026.

For updates and more information on how One Big Beautiful Bill impacts student loans and borrowers, please visit One Big Beautiful Bill Act Updates | Federal Student Aid.

For more information on private loans, please visit FastChoice.

While Belmont University does not endorse or recommend one specific private loan lender, FastChoice offers a list of lenders that have been used by Belmont University students within the past three years. If you are interested in a lender not on this list, simply contact that lender directly or visit their website for more detailed information.